The EU Deforestation Regulation Is Live for Coffee: What Changes in 2026

The EUDR took effect for coffee at the end of 2025. What the rules mean for traceability, prices, and what shows up on your bag in Europe.

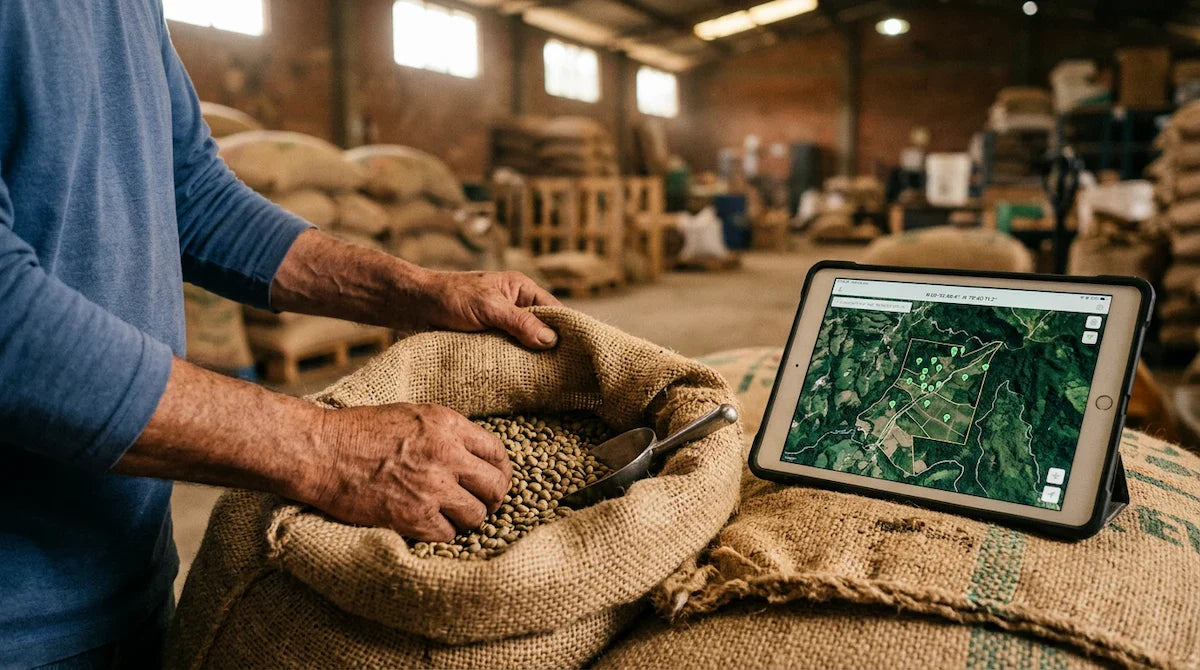

An importer at the port of Antwerp opens a tablet next to a container of green coffee from Honduras. Before customs clears the shipment, she pulls up a satellite map. Red dots mark every plot of origin. A due-diligence statement sits attached to the file. If one coordinate falls inside a polygon flagged as post-2020 deforestation, the container does not move.

This is the EU deforestation regulation coffee reality in 2026. After a one-year delay, the EUDR coffee impact is no longer theoretical. The rules are live, the customs systems are running, and the first containers are being held back.

What the EUDR actually requires for coffee

The EU Deforestation Regulation took effect for large operators on 30 December 2025. SMEs follow on 30 June 2026. It covers seven commodities: cattle, cocoa, coffee, palm oil, rubber, soy, and wood. Every kilo of green coffee entering the EU must come with GPS coordinates of the farm plot it came from, plus a due-diligence statement confirming no deforestation occurred on that plot after 31 December 2020.

Coffee traceability rules used to mean a name on a sack and a story on a website. Now they mean polygon data, satellite cross-checks, and a paper trail that connects every gram in the bag to a specific piece of land. The EU is the largest coffee market in the world, taking in roughly 33% of global green coffee imports, so the rules effectively set a new global standard.

Why smallholder origins are hit hardest

Roughly 12.5M smallholder coffee farmers produce most of the world's coffee. Many of them work plots under 2 hectares, in regions with patchy internet and no land registry. Asking them to provide coffee geolocation data on their own is, for now, unrealistic. The burden falls on cooperatives, importers, and government extension programs to do the mapping for them.

The cost adds up. Compliance estimates for coffee supply chain compliance range from €0.10 to €0.50 per kilo of green coffee, depending on origin and infrastructure. For smallholder coffee farmers selling at $3 per kilo, that is a real cut. The Specialty Coffee Association has documented the risk that some smallholder origins simply exit the EU market rather than absorb the compliance burden, which is the opposite of what the regulation set out to achieve.

What European roasters and shops are doing

Large roasters started building EUDR systems two years ago. They have software, suppliers, and dedicated compliance teams. Small specialty roasters with direct relationships at origin already had most of the data, just not in the right format. The work for them has been administrative, not structural.

The middle of the market is where it gets harder. Mid-size roasters buying through brokers without farm-level traceability are scrambling to either switch suppliers or pay for retroactive mapping. Some have narrowed their origin lists. A few have pulled certain lots off shelves entirely while the paperwork catches up.

What consumers will notice in 2026

Two things will show up on EU coffee imports this year. First, prices on origin-traced bags will edge upward, because the compliance cost lands somewhere. Specialty bags should absorb €0.10 to €0.30 per 250g in most cases. Cheap commodity-blend coffee in supermarkets may see less of a hit because the volume spreads the cost thin.

Second, bags will get more specific. Expect to see farm names, GPS coordinates, harvest dates, and processing details on packaging that used to just say "Colombia" or "blend." Coffee certification labels will still exist, but EUDR compliance is now the baseline. Certification has to offer something extra to justify its place on the bag.

Drink the coffee behind the writing

Freshly roasted, delivered to your door, with a fair deal behind every bag.